- The commissions/incentives should only be paid out on the retail of product/s.

- No charge/fees for enrolment.

- No commissions/incentives or rewards should be given/offered to the direct sellers for enrolment of new direct sellers.

- Payment of Incentives/Commission - The payment of commissions/incentives should be made without fail and delay as per the commitments of the compensation plan followed by the company.

- The company should not provide commitments of returns on investment/s (on purchase of product/s or without the purchase of product/s) in the form of interest, salary, loan, help, donation, market development fees and support fund to/through the direct sellers, to any individual/s.

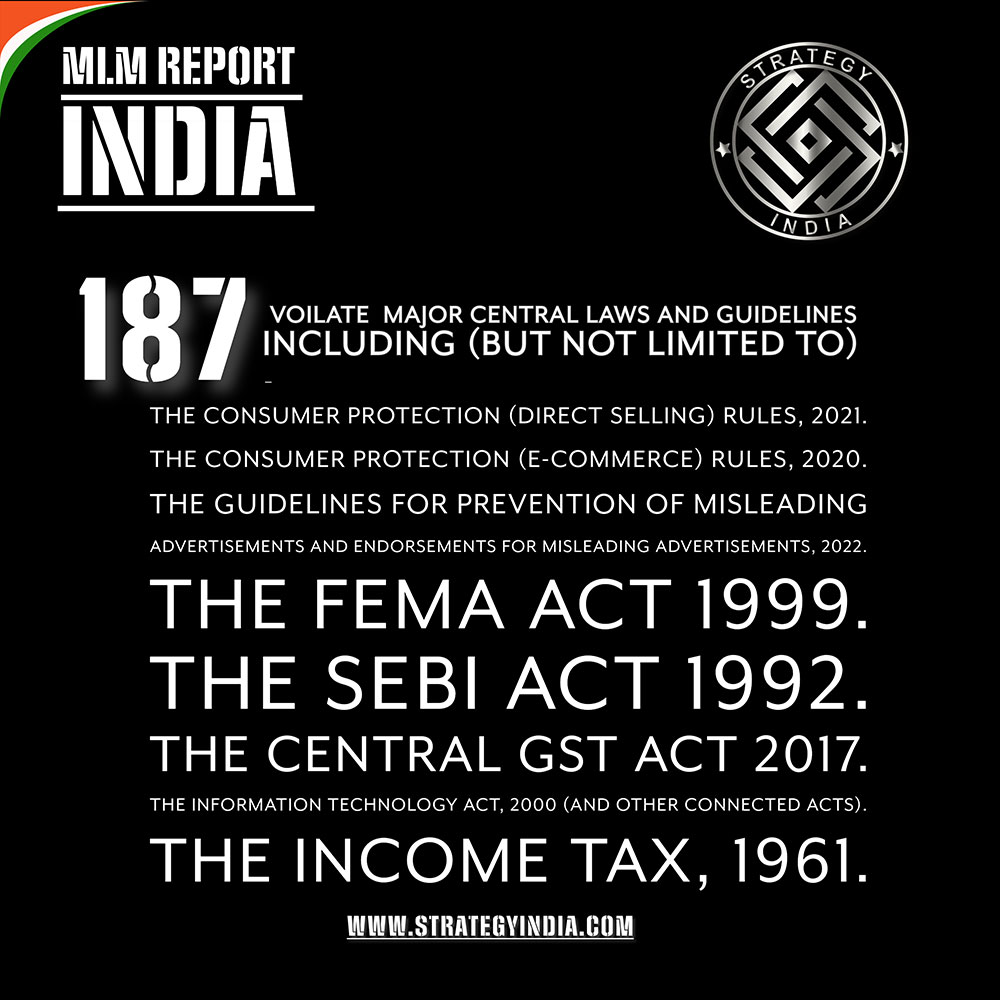

- The company should deduct (Tax deducted at source) from the pay-outs to the direct sellers

- TDS @ 10% in case of availability of the PAN details of the direct sellers.

- TDS @ 20% in the event of non-availability of PAN details